By alphacardprocess March 3, 2026

Same-day funding can feel like a small operational upgrade—until you live through a week of lab invoices, payroll, supply orders, and a few unexpected refunds hitting at the same time. Then it becomes clear: getting your card deposits sooner isn’t just “nice to have.” It can be the difference between running calmly and constantly playing catch-up.

As a dental payments and merchant services consultant, I’ve seen front desks do everything right—collecting at time of service, running clean end-of-day routines, and following strong refund practices—yet still get surprised by funding delays. The reason is simple: many practices don’t realize how many steps exist between a card being approved and money actually posting to the bank.

This guide walks you through setting up same-day funding for dental practices in a practical, people-first way. You’ll learn how same-day funding really works, how it differs from similar “fast money” claims, what makes a practice eligible, and how to implement it without disrupting your front-desk workflow.

You’ll also get a rollout plan, optimization plan, troubleshooting steps, and a checklist you can hand to your team.

What Same-Day Funding Actually Means (And What It Doesn’t)

Same-day funding means your card processor releases your approved card sales to your bank on the same business day—assuming you meet the provider’s cut-off time and your transactions clear required checks. The key phrase is “releases funds,” because the moment money posts to your bank account can still depend on your bank’s internal posting schedule.

It’s easy to confuse same-day funding with other terms that sound similar. Here’s the clean way to think about it:

- Same-day funding: Your processor initiates the deposit the same day you run/close the batch (by a cut-off time).

- Same-day settlement: Card networks and acquiring systems settle transactions the same day; this can happen even if you’re funded later.

- Next-day deposits: Deposits arrive the next business day (common for many standard merchant accounts).

- Instant payouts: A fast transfer to a debit card or wallet-like balance, often with additional fees and different risk controls.

Same-day funding isn’t magic. It’s a deposit schedule advantage supported by underwriting, bank verification, and disciplined daily batch habits. When those pieces align, dental payment processing with same-day funding can be a reliable cash-flow tool. When they don’t, it can become a source of frustration.

Same-Day Funding vs Settlement vs “Instant Payouts”

A dental card payment takes a multi-step journey. Different companies use different words for each step, which is why expectations get confused. The cleanest explanation is to separate these phases:

- Authorization: The card is approved at the time of charge.

- Batching: Transactions are grouped together for the day (often via batch close).

- Settlement: The card networks and acquiring bank finalize the movement of funds between banks.

- Funding: Your processor releases the deposit to your bank.

- Bank posting: Your bank makes the deposit available in your account.

Same-day settlement is not the same as same-day funding. A transaction could settle quickly, but your processor might still fund you on a standard schedule (like next-day). On the flip side, a processor may initiate same-day funding based on its own risk models, even though settlement is still happening in the background.

“Instant payouts” typically use separate methods that move money to a debit card or internal balance quickly. They can be helpful in some industries, but dental offices often prefer predictable business-account deposits and clean reconciliation reporting over speed-at-any-cost.

Who Offers Same-Day Funding (And Why Not Every Practice Qualifies)

Same-day funding is typically offered by a combination of:

- Payment processors that manage merchant accounts, underwriting, and the deposit schedule.

- Acquiring banks that support card acceptance and settlement relationships.

- Payment facilitators (in some setups) that onboard practices under a master arrangement and manage risk centrally.

Not every practice qualifies because same-day funding increases risk for the provider. When a processor funds you early, it may be advancing money before all settlement processes and risk checks are fully complete. That’s why eligibility often depends on a practice’s transaction profile and documentation readiness.

Common reasons an office may not qualify at first include:

- Limited processing history or a recent account opening.

- High refund rates, inconsistent ticket sizes, or unusual transaction patterns.

- A higher-than-normal proportion of keyed or phone transactions.

- Bank account verification issues or mismatched business details.

- Prior funding delays, disputes, or elevated chargeback ratio trends.

Same-day funding tends to be easier to approve when the practice has stable volume, predictable transaction behavior, and clear ownership documentation. Newer practices can still qualify, but they usually need cleaner setup, stronger controls, and sometimes a gradual ramp-up period.

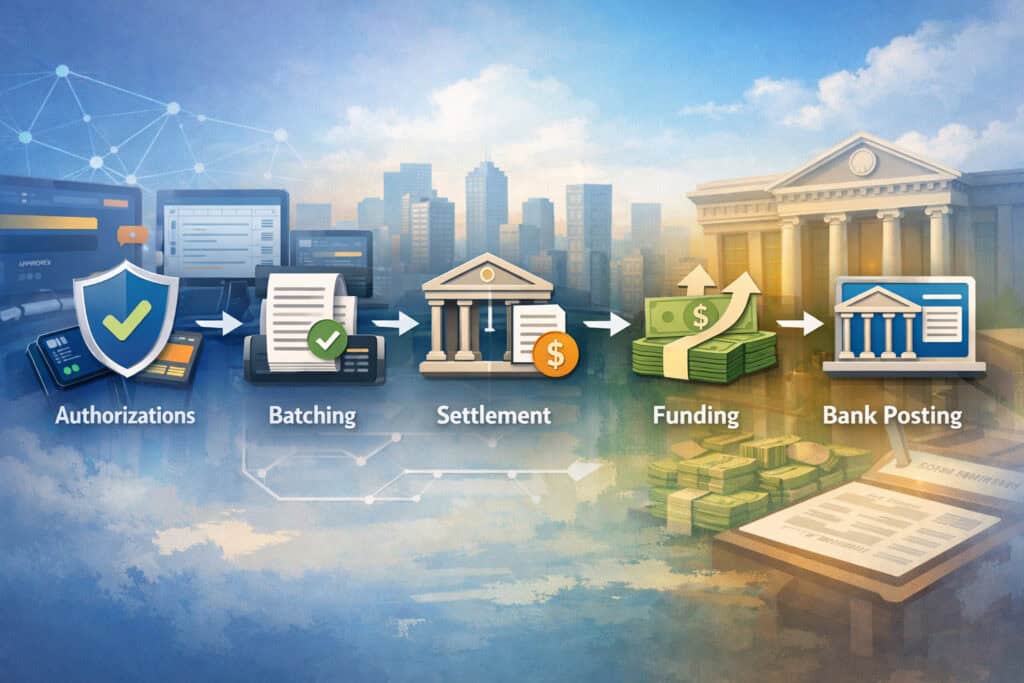

How the Money Moves: Authorizations → Batching → Settlement → Funding → Bank Posting

Let’s walk through the mechanics as your front desk experiences them, without the jargon.

Authorization: The “Approved” Message

When a patient pays in person, over the phone, or via an online payment link, the terminal or gateway sends an authorization request. If approved, it means funds are available and the card details are valid enough to proceed. It does not mean you’ve been paid yet.

For dental offices, this is where common workflow differences matter:

- EMV chip transactions are generally stronger from a risk perspective.

- Keyed or phone payments can be legitimate but may trigger more risk monitoring.

- Online payment links can be smooth for patients but require clean gateway configuration.

At this stage, your receipt prints, your practice management system records the payment, and the patient leaves feeling settled. Behind the scenes, you’re still at the beginning of the money movement process.

Batching and Batch Close: The Step That Quietly Controls Your Deposit Speed

Most dental card transactions sit in an “open batch” until your system closes it. Some systems auto-close at a set time; others require a manual end-of-day action. If the batch doesn’t close properly, the day’s approved sales can miss settlement windows and therefore miss funding windows.

Batch close is one of the biggest operational causes of funding delays. It’s also one of the easiest things to fix with good training and daily routines.

Here’s what front-desk staff should know:

- Closing the batch is not “optional admin.” It’s what triggers the money movement.

- If you close after the funding cut-off times, your deposit can shift to next-day.

- If you have multiple terminals or channels (in-office + virtual terminal + online links), each may have its own batch behavior.

Settlement vs Funding: Where Many Delays Hide

Settlement is where the acquiring bank and card networks finalize the exchange. Funding is when the processor releases money to your bank.

Delays can happen between these steps for reasons like:

- Transactions flagged for review (unusual ticket size, unusual volume, higher-risk entry method).

- Incomplete bank account verification or changes in business details.

- Risk monitoring alerts triggered by refund spikes or dispute activity.

- Late batch closure or multiple batches closing inconsistently.

The more consistent your transaction patterns and the cleaner your end-of-day routines, the less likely you are to hit these delays.

Bank Posting: Your Bank Has the Final Say on “Available Today”

Even when a processor initiates same-day funding, your bank may post deposits on a schedule. Some banks post throughout the day; others post in batches, and weekend/holiday funding may behave differently.

This is why “same-day funding” should be evaluated as a whole chain:

- Processor cut-off time met?

- Deposit initiated?

- The bank posted it?

- Funds available for use?

Why Same-Day Funding Matters for Dental Cash Flow (And When It Isn’t Worth It)

Dental practices are unique because revenue timing is split across patient payments, insurance reimbursements, and financing or payment plans. Same-day funding doesn’t solve everything, but it can stabilize the part you control most: card-based collections.

Here are practical benefits I see repeatedly:

- Payroll timing relief when payroll lands before deposits would normally post.

- Lab bill flexibility, especially for high-ticket cases that involve outside work.

- Supply ordering confidence, reducing last-minute “hold off on ordering” stress.

- Multi-location visibility, where centralized finance needs predictable deposit schedules.

- Cleaner cash forecasting, because deposits become more consistent day-to-day.

Same-day funding can also reduce the mental load on administrators. They spend less time checking for deposits and more time managing real operational priorities.

That said, it’s not always worth the cost. Situations where you should think twice:

- If your volume is small and you rarely feel cash pressure.

- If the provider charges early funding fees that outweigh the operational benefits.

- If your practice has frequent refunds, cancellations, or high dispute exposure.

- If your bank posting habits make same-day less meaningful (for example, deposits post late evening regardless).

Eligibility and Underwriting: What Providers Look At (And How to Prepare)

To qualify for same-day funding for dental practices, you’re being evaluated like a partner in risk. Underwriting and KYC checks aren’t just paperwork; they determine whether a provider trusts your deposit schedule to move faster.

Transaction History and Stability

Providers prefer predictable behavior:

- Stable monthly volume without sharp spikes.

- Consistent average ticket size.

- A healthy mix of in-person EMV transactions.

- Low dispute and chargeback ratio trends.

If your office has seasonal spikes or sudden jumps due to a new service line, that doesn’t mean you can’t qualify. It means you need transparency and strong documentation.

Refund and Chargeback Patterns

Refunds happen in dentistry. Treatment plans change. Insurance estimates differ. Patients reschedule. Underwriters know this.

What they watch for is pattern risk:

- Refund spikes after large-volume days.

- Large refunds outside normal business hours.

- High refund-to-sales ratios.

- Disputes tied to unclear refund policy or unclear authorization.

A clear, documented refund policy—explained to patients before charging—reduces both chargebacks and risk flags.

Average Ticket, Entry Method, and Channel Mix

Dental offices can have high-ticket transactions. That’s normal. But it increases scrutiny.

Underwriters look at:

- How many large tickets you run and how often.

- Whether large tickets are chip-present or keyed.

- Whether phone payments are supported by appropriate verification and staff procedures.

- Whether online payment links are properly configured and tied to patient records.

A high keyed percentage doesn’t automatically disqualify you, but it can reduce how “same-day” your same-day funding behaves if risk monitoring frequently pauses deposits.

Business Documentation and KYC

Expect to provide:

- Business identity documentation.

- Ownership and control information for KYC.

- Bank account verification details.

- Supporting documentation if your practice name differs from the bank account name.

If your provider asks for documentation, treat it like a funding-critical project. Slow document responses are a common reason accounts remain on slower deposit schedules.

Bank Account Health and Verification

Bank account verification is more than “enter routing and account number.” Providers watch for:

- Name matching between legal business name and bank account title.

- Bank account changes and how often they happen.

- Returned deposits or failed ACH deposits.

- Any mismatch errors that cause funding delays.

Step-by-Step: Setting Up Same-Day Funding for Dental Practices

This section is your practical setup map. The exact steps vary slightly by provider, but the workflow is consistent.

Step 1: Choose Dental Merchant Services With Same-Day Funding That Matches Your Workflow

Not all “fast funding” offers are designed for the way dental offices operate. You want a provider that understands:

- Multiple payment channels (in-office, phone, online links).

- Refund scenarios tied to treatment changes.

- Split tender and deposits.

- Reconciliation reporting that works for office managers and administrators.

When comparing providers, use a checklist mindset:

- Do they offer same-day funding as a standard deposit schedule or as an add-on?

- Are there early funding fees or special conditions?

- What are the funding cut-off times?

- How do they handle weekend/holiday funding?

- What tools support daily reconciliation reporting?

Avoid picking solely on “speed.” A fast deposit paired with poor reporting can create hours of admin work. For most practices, the best provider is the one that delivers predictable deposits and easy reconciliation.

Step 2: Confirm Funding Cut-Off Times and Batch Close Procedures

Cut-off times are the make-or-break detail. Same-day funding usually requires:

- Batch close completed by a specific time.

- Transactions captured successfully before that time.

- No risk flags that pause funding.

Make sure you understand:

- The exact cut-off time (and whether it is based on your local time).

- Whether cut-off times differ by payment channel (terminal vs gateway).

- Whether your system auto-batches or requires a manual step.

- How to confirm the batch closed successfully.

You should also ask how exceptions work. If you miss a cut-off by a few minutes, does your deposit automatically shift to next-day deposits, or is there a grace window?

Step 3: Verify Your Bank Account Correctly and Avoid Mismatch Errors

Bank account verification errors are one of the most common causes of funding delays. Even when everything else is perfect, a mismatch can trigger a hold until the provider re-verifies.

To avoid that:

- Use the correct legal business name consistently.

- Ensure the bank account title matches the business identity.

- Provide clear documentation (bank letter or voided check).

- Confirm ownership details are correct for underwriting and KYC.

If your practice operates under a brand name that differs from the legal business name, this is normal—but it must be documented properly. Otherwise, you can end up in a “manual review” loop that delays funding.

Also confirm whether deposits are sent via ACH deposits and what bank posting behavior is typical. It’s not enough for the processor to send the deposit; you want it available when you need it.

Step 4: Configure Terminals, Gateways, and Payment Links for Consistent Capture

Most dental offices process through multiple tools:

- POS terminal in the office for card-present payments.

- Virtual terminal for phone payments.

- Payment gateway for online payment links.

- Recurring payments for payment plans or membership-style billing.

Each channel must be configured with:

- Correct merchant account credentials.

- Tokenization settings where applicable.

- Proper receipt and descriptor configuration.

- Consistent batch behavior.

If you use online payment links, confirm how they batch. Some systems batch separately from in-office terminals. That can cause confusion when deposits arrive in multiple chunks.

Also consider whether tips/gratuity applies in your workflow. Some practices accept tips for optional services, while others avoid them. If tips are used, ensure tips are adjusted and finalized before batch close, or your totals can be off.

Step 5: Train Staff on Daily Batching, Refunds, and Dispute-Reducing Habits

Same-day funding lives or dies at the front desk. Training isn’t about turning staff into payment experts. It’s about consistent habits.

Focus training on:

- What “batch close” means and who owns it.

- How to confirm the batch closed successfully.

- When to use refunds vs voids (and which keeps reconciliation cleaner).

- How to document patient consent and payment plan terms.

- How to handle phone payments with consistent verification steps.

Refund handling matters because it affects both cash flow and risk monitoring. A practice that processes refunds carefully and consistently is less likely to trigger funding reviews.

Step 6: Set Up Reporting and Reconciliation That an Office Manager Can Actually Use

If deposits arrive faster but your reporting is messy, your admin workload increases. You want reconciliation reporting that helps you answer:

- Which days and batches created which deposits?

- Are deposits split by channel or location?

- What fees were deducted and why?

- What refunds and chargebacks affected the deposit?

Look for a dashboard that provides:

- Batch reports and transaction details.

- Deposit schedule visibility.

- Funding status and timestamps.

- Exportable reports that match your accounting workflow.

For multi-location practices, insist on location-level reporting. Otherwise, you’ll spend too much time untangling which site produced which totals.

Fees and Contract Terms: Pricing Models, Questions to Ask, and Red Flags

Same-day funding is rarely “free,” but pricing should be understandable. You should also be able to evaluate whether the costs match your practice’s real value from faster deposits.

Common Pricing Models You Might See

Providers may price same-day funding in different ways, such as:

- An add-on fee for early funding access.

- A different rate plan tied to funding speed.

- A tiered setup where certain volume levels qualify for better deposit schedules.

- A blended approach that combines processing fees and funding schedule terms.

Be cautious about anyone who avoids discussing how early funding fees work. Transparency is a major trust signal.

Questions to Ask Before You Sign

Use these questions to keep the conversation grounded:

- What are the exact funding cut-off times, and are they different for different channels?

- What happens if we miss the cut-off time?

- How are weekend/holiday funding and bank posting handled?

- Under what conditions can funding be delayed or held?

- Is there a reserve account requirement, and how is it calculated?

- Are there termination fees or long contract terms?

- Can you provide funding status reporting and reconciliation reporting examples?

Red Flags That Often Lead to Funding Pain

Watch for these warning signs:

- Vague promises like “instant deposits” without clear deposit schedule details.

- A provider that cannot explain settlement vs funding.

- High-pressure sales tactics that avoid underwriting questions.

- Hidden reserve account clauses or unexplained risk monitoring triggers.

- Contract terms that allow broad funding holds without clear reasons.

- Difficult cancellation terms or sudden termination fees.

Risk and Compliance: Protecting Same-Day Funding From Interruptions

Same-day funding is a privilege your provider extends based on trust and monitoring. Protecting that trust requires operational discipline. The good news is most best practices also improve patient experience and reduce disputes.

Chargebacks and Dispute Prevention

Chargebacks in dental practices often come from misunderstandings rather than fraud. Common triggers include:

- Confusion about treatment plans or deposits.

- Refund expectations not explained clearly.

- Billing descriptor not recognized by the patient.

- Unclear documentation for prepayments or cancellations.

To prevent chargebacks:

- Use clear receipts and consistent descriptors.

- Document consent for large-ticket charges.

- Have a written refund policy communicated upfront.

- Respond quickly to disputes with complete documentation.

A rising chargeback ratio is a fast way to lose same-day funding privileges. Even a small number of disputes can matter if your volume is low.

Fraud Controls, Keyed Payments, and Risk Monitoring

Phone payments and keyed transactions are common in dentistry. They’re not automatically a problem, but they require consistent controls.

Best practices include:

- Using a virtual terminal with built-in verification features.

- Ensuring the billing address and contact details match patient records.

- Avoiding manual overrides unless necessary.

- Not splitting transactions unnaturally to force approvals.

Risk monitoring systems look for patterns. If your office has inconsistent entry habits, you can trigger holds even when everything is legitimate.

PCI Compliance, Tokenization, and Secure Storage

PCI compliance matters because poor security practices can lead to data exposure, reputational harm, and processor action. For practical purposes:

- Don’t store card numbers in patient notes or spreadsheets.

- Use tokenization for recurring payments.

- Use approved payment gateways and secure payment links.

- Keep staff access controlled and audited.

Tokenization is especially helpful for payment plans. It allows you to process recurring payments without storing sensitive card data directly.

Refund Policy and Handling to Avoid Funding Holds

Refund behavior is monitored because it changes risk exposure. A thoughtful refund process includes:

- Linking refunds to the original transaction.

- Avoiding excessive same-day refunds that look suspicious.

- Using voids when appropriate and within allowed timeframes.

- Getting patient acknowledgment for refund timelines.

Refund timelines should be communicated clearly so patients don’t file disputes out of impatience.

Real-World Scenarios: How Same-Day Funding Plays Out in Dentistry

Same-day funding sounds straightforward, but how it behaves depends on how your office collects payments. These scenarios reflect what I see most often.

Scenario 1: Single-Location Practice With Consistent Chairside Collections

A single-location practice processing mostly in-person EMV transactions typically qualifies faster. The workflow is simpler:

- One primary terminal.

- One batch close routine.

- Fewer deposit splits.

The main challenge is usually training and consistency. Once the team reliably closes batches before the cut-off time, same-day funding becomes predictable.

What to watch:

- Occasional high-ticket days that spike volume.

- Refunds tied to treatment plan changes.

- Phone payments for last-minute balances.

Scenario 2: Multi-Location Practice With Centralized Finance

Multi-location groups often have:

- Multiple terminals per location.

- Shared payment links and gateways.

- Centralized reconciliation reporting needs.

Same-day funding can be very beneficial here, but only if reporting is strong. Otherwise, the finance team spends hours matching deposits across locations.

Key considerations:

- Location-level reporting and deposit tagging.

- Standardized batch close responsibilities per site.

- Consistent procedures for keyed payments and payment plans.

The biggest pitfall is inconsistent training. If one location misses a batch close regularly, deposits become unpredictable and the group loses confidence in the process.

Scenario 3: High-Ticket Procedures and Large Prepayments

High-ticket procedures raise underwriting scrutiny because large amounts can be disputed or refunded. Same-day funding may still be possible, but you should expect:

- More frequent risk monitoring checks.

- Occasional funding delays if patterns shift suddenly.

- Higher documentation expectations.

To keep funding stable:

- Document patient authorization and treatment details.

- Avoid unusual splitting of large charges.

- Use clear payment plan agreements when applicable.

If the provider offers tools for preauthorization or secure capture of patient consent, use them. This is where operational discipline directly reduces risk.

Scenario 4: Heavy Payment-Plan Usage With Recurring Payments

Payment plans are common, but they introduce complexity:

- Recurring payments can trigger declines and customer confusion.

- Refunds may be partial and frequent.

- Tokenization and secure gateway configuration become essential.

Same-day funding can still work well here, especially if the system supports tokenization, clear recurring receipts, and clean reconciliation reporting.

The biggest risk is mismanaging card data or changing terms without patient agreement, which can increase disputes.

Scenario 5: Mixed In-Person, Phone Payments, and Online Payment Links

This is the most common “modern dental office” setup. It can absolutely qualify for same-day funding, but only if channels are aligned:

- Same merchant account structure.

- Consistent entry policies.

- Unified reporting.

Otherwise, you’ll see deposit splits, mismatched totals, and risk flags.

The fix is usually not technical—it’s a process. Pick a standard method for each payment type and train everyone to follow it.

A Practical 30-Day Rollout Plan

Same-day funding shouldn’t be rolled out as a surprise switch. The goal is minimal disruption and maximum consistency.

Days 1–7: Setup and Validation

In the first week:

- Choose the provider and confirm same-day funding terms in writing.

- Complete underwriting and KYC documentation promptly.

- Confirm bank account verification and deposit schedule.

- Configure terminals, payment gateway, virtual terminal, and online payment links.

- Create a written end-of-day batch close checklist.

During this phase, expect some back-and-forth with underwriting. Respond fast and keep documentation organized.

Days 8–14: Staff Training and Soft Launch

In week two:

- Train staff on batch close and daily confirmation steps.

- Train refund handling: void vs refund, documentation, and timing.

- Set expectations for what “same-day” means and how bank posting works.

- Run a soft launch with daily reconciliation reporting.

Your goal is to catch issues early while volume is manageable.

Days 15–21: Full Launch With Daily Reconciliation

In week three:

- Go live fully across all channels.

- Reconcile deposits daily against batch reports.

- Track cut-off time performance and missed batches.

- Monitor refunds and chargeback ratio trends.

If deposits are split, document why. Split deposits are not inherently bad, but they must be predictable.

Days 22–30: Stabilize and Document

In week four:

- Finalize your standard operating procedures.

- Build a “funding troubleshooting” cheat sheet for staff.

- Confirm weekend/holiday funding behavior.

- Review any risk monitoring flags with your provider.

By day 30, the process should feel routine. If it doesn’t, the problem is usually one of these: batch close inconsistency, bank mismatch issues, or unclear refund practices.

A 90-Day Optimization Plan to Keep Funding Fast and Reliable

Once same-day funding is working, your goal is to protect it. Optimization is about consistency, controls, and visibility.

Days 31–60: Improve Controls and Reduce Exceptions

Focus on:

- Reducing keyed transactions where possible by using payment links or in-person EMV.

- Tightening refund documentation and approval steps.

- Standardizing descriptor and receipt messaging.

- Reviewing weekly reconciliation reporting for anomalies.

Look for patterns like:

- A specific day of week when batch closes are missed.

- Refund spikes following particular procedures.

- One staff member’s transactions triggering more risk reviews.

Days 61–90: Strengthen Reporting and Forecasting

In this phase:

- Set up more automated reporting exports for accounting.

- Build a cash-flow view that separates settlement vs funding timing.

- Confirm reserve account terms (if any) and track how they’re applied.

- Review chargeback and dispute response routines.

Also evaluate whether early funding fees still make sense. Once operations stabilize, you may find that next-day deposits are sufficient—or you may confirm that same-day funding continues to deliver real value.

Troubleshooting: Why Deposits Don’t Arrive Same Day (And How to Fix It)

Even with same-day funding enabled, deposits can sometimes arrive later. Here are the most common causes and practical fixes.

Missed Cut-Off Times or Late Batch Close

Symptoms: Deposit shifts to next-day deposits even though sales were completed.

Fix:

- Confirm the cut-off time and your actual batch close timestamp.

- Set batch close reminders earlier than the cut-off by a buffer window.

- Ensure auto-close is enabled if available and reliable.

Batch Didn’t Close Successfully

Symptoms: Transactions show approved, but they remain in an open batch.

Fix:

- Train staff to confirm batch close success (receipt, screen confirmation, or report).

- Check for terminal connectivity issues.

- Ensure each terminal or channel is included in the closing routine.

Bank Account Verification or Mismatch Errors

Symptoms: Funding delays, returned deposits, or a request for additional bank documentation.

Fix:

- Verify account title matches legal business identity.

- Provide updated bank letter/voided check.

- Avoid changing bank accounts mid-rollout.

Risk Monitoring Flags

Symptoms: Funding is delayed after unusual volume spikes or large-ticket days.

Fix:

- Notify your provider in advance of expected volume increases when possible.

- Document large-ticket transactions thoroughly.

- Reduce inconsistent patterns (for example, sudden spikes in keyed transactions).

Refund or Chargeback Activity Triggering Holds

Symptoms: Funding slows during periods of higher refunds or dispute activity.

Fix:

- Review refund policy communication and documentation.

- Respond quickly to disputes with complete records.

- Consider internal approval for large refunds to prevent accidental spikes.

Weekend and Holiday Funding Behavior

Symptoms: Deposits expected “same-day” don’t appear during weekends/holidays.

Fix:

- Confirm whether same-day funding applies only to business days.

- Ask for the provider’s weekend/holiday funding policy.

- Align expectations with your bank’s posting schedule.

FAQ

Q1) What does “setting up same-day funding for dental practices” actually involve?

Answer: It involves choosing a processor that offers same-day deposits, completing underwriting and KYC, verifying your bank account, configuring your terminals and payment gateway, and training staff to close batches consistently before the funding cut-off times.

Q2) Is same-day funding the same as instant payouts?

Answer: No. Same-day funding typically means the processor initiates an ACH deposit to your bank the same business day. Instant payouts often use a different method, may cost more, and can come with different risk controls and limitations.

Q3) Why do some practices get approved and others don’t?

Answer: Approval depends on underwriting factors like transaction history, chargeback ratio, refund behavior, average ticket, channel mix (EMV vs keyed), documentation completeness, and bank account verification reliability.

Q4) What are funding cut-off times, and why do they matter?

Answer: Cut-off times are the latest time you can close a batch and still qualify for same-day funding. If you close after the cut-off, your deposit may shift to next-day deposits even if transactions were approved earlier.

Q5) What’s the difference between settlement vs funding?

Answer: Settlement is when card networks and the acquiring bank finalize transaction movement. Funding is when your processor releases the deposit to your bank. A transaction can be settled even if funding arrives later, and vice versa depending on the provider’s model.

Q6) Can multi-location practices use same-day funding effectively?

Answer: Yes, but success depends on consistent end-of-day routines at each site and strong reconciliation reporting. Location-level reporting is especially important to avoid confusion and time-consuming deposit matching.

Q7) How do refunds affect same-day funding?

Answer: Refunds can trigger risk monitoring if patterns look unusual or if refund volume spikes. Clear refund policies, consistent documentation, and careful refund processing reduce funding interruptions.

Q8) Will same-day funding work for online payment links and virtual terminal payments?

Answer: It can, but you must confirm how those channels batch and whether they share the same funding schedule. Misconfigured gateways or separate batching can lead to split deposits and reconciliation headaches.

Q9) Do weekends and holidays count for same-day funding?

Answer: Often, same-day funding is limited to business days, and weekend/holiday funding may follow different rules. Your bank posting schedule also impacts when deposits become available.

Q10) Are early funding fees always worth it?

Answer: Not always. It depends on your cash-flow needs and whether faster deposits prevent real operational problems. Evaluate the value during tight cash weeks—like payroll or heavy lab-bill periods—rather than judging purely on convenience.

Q11) What is a reserve account, and should I worry about it?

Answer: A reserve account is a risk control where a portion of funds may be held temporarily to cover potential chargebacks or refunds. Reserves aren’t always required, but unclear reserve terms are a red flag. If a reserve is proposed, ask how it’s calculated, how long it lasts, and when it’s released.

Q12) What should we do if a same-day deposit doesn’t arrive?

Answer: First, confirm batch close and cut-off compliance. Next, request funding status confirmation from the processor. If the processor initiated funding, then ask your bank about posting timing. If not, investigate bank verification issues, risk monitoring flags, or refund/chargeback activity.

Conclusion

Same-day funding can be a powerful upgrade for a dental office—especially when your practice depends on predictable deposits to cover payroll, lab bills, supplies, and multi-location coordination.

But the real success factor isn’t the marketing promise. It’s the operational reality: clean underwriting setup, accurate bank verification, consistent batch close, and disciplined refund practices.

When done correctly, same-day funding for dental practices improves cash-flow control without forcing your team to become payment experts. The goal is simple: give your front desk a workflow that’s easy to follow and give your administrators deposits and reporting they can trust.